UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(mark one)

☒ Annual Report Pursuant To Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended September 30, 2018

or

☐ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from _______________ to _______________

Commission file number 001-35527

MYnd Analytics, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 87-0419387 |

| (State or other jurisdiction | (I.R.S. Employer |

| of incorporation or organization) | Identification No.) |

26522 La Alameda, Suite 290

Mission Viejo, CA 92691

(Address of Principal Executive Offices)(Zip Code)

(949) 420-4400

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered |

| Common Stock, $0.001 par value | The Nasdaq Stock Market LLC |

| Warrants to Purchase Common Stock | The Nasdaq Stock Market LLC |

Securities registered under Section 12(g) of the Exchange Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer | ☐ |

| Non-accelerated filer ☐ | Smaller reporting company | ☒ |

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.) Yes ☐ No ☒

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant on March 31, 2018, the last business day of the registrant's most recently completed second fiscal quarter was $5,193,530 (calculated based on the price at which the registrant's common stock was last sold on that date).

As of December 10, 2018, the registrant had 7,555,004 shares of common stock, $0.001 par value, issued and outstanding.

MYND ANALYTICS, INC.

2018 FORM 10-K ANNUAL REPORT

TABLE OF CONTENTS

1

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K for the fiscal year ended September 30, 2018, including the sections entitled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business,” contain certain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that include information relating to future events, future financial performance, strategies, expectations, competitive environment, regulation and availability of resources. These forward-looking statements include, without limitation, statements regarding: proposed new products or services; our statements concerning litigation or other matters; statements concerning projections, predictions, expectations, estimates or forecasts for our business, financial and operating results and future economic performance; statements of management’s goals and objectives; trends affecting our financial condition, results of operations or future prospects; our financing plans or growth strategies; and other similar expressions concerning matters that are not historical facts. Words such as “may,” “will,” “should,” “could,” “would,” “predicts,” “potential,” “continue,” “expects,” “anticipates,” “future,” “intends,” “plans,” “believes” and “estimates” and similar expressions, as well as statements in future tense, identify forward-looking statements.

Forward-looking statements should not be read as a guarantee of future performance or results and will not necessarily be accurate indications of the times at, or by which, that performance or those results will be achieved. Forward-looking statements are based on information available at the time they are made and/or management’s good faith belief as of that time with respect to future events and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause these differences include, but are not limited to:

| • | our need for immediate additional funding to support our operations and capital expenditures; |

| • | our ability to successfully maintain listing of our shares of common stock on the Nasdaq Capital Market; |

| • | our history of operating losses; |

| • | our inability to gain widespread acceptance of our PEER Reports; |

| • | our inability to prevail in convincing the United States Food and Drug Administration (the “FDA”), that our rEEG or PEER Online service does not constitute a medical device and should, therefore, not be subject to regulations; |

| • | the possible imposition of fines or penalties by the FDA for alleged violations of its rules and regulations; |

| • | our subsidiary in telebehavioral health may be harmed by evolving governmental regulation; |

| • | our telebehaviorial health subsidiary's business model requires work with affiliated professional entities not owned by the Company; |

| • | our telebehaviorial health subsidiary may require an expanded and maintained network of certified professionals; |

| • | our revenue and prospects for profitability may be harmed; |

| • | our business may be subject to additional regulations in the future that could increase our compliance costs; |

| • | our operating results may fluctuate significantly and our stock price could decline or fluctuate if our results do not meet the expectation of analysts or investors; |

| • | our inability to achieve greater and broader market acceptance of our products and services in existing and new market segments; |

| • | any negative or unfavorable media coverage; |

| • | our inability to generate and commercialize additional products and services; |

| • | our inability to comply with the substantial and evolving regulation by state and federal authorities, which could hinder, delay or prevent us from commercializing our products and services; |

| • | our inability to successfully compete against existing and future competitors; |

| • | delays or failure in clinical trials; |

2

| • | any losses we may incur as a result of litigation; |

| • | our inability to manage and maintain the growth of our business; |

| • | our inability to protect our intellectual property rights; |

| • | employee relations; |

| • | possible security breaches; |

| • | possible medical liability claims; |

| • | possible personal injury claims in the future; and |

| • | our limited trading volume. |

Additional risks, uncertainties and other factors that may cause our actual results, performance or achievements to be different from those expressed or implied in our written or oral forward-looking statements may be found under “Risk Factors” contained in this Annual Report.

Forward-looking statements speak only as of the date they are made. You should not put undue reliance on any forward-looking statements. We assume no obligation to update forward-looking statements to reflect actual results, changes in assumptions or changes in other factors affecting forward-looking information, except to the extent required by applicable securities laws. If we do update one or more forward-looking statements, no inference should be drawn that we will make additional updates with respect to those or other forward-looking statements.

Introduction

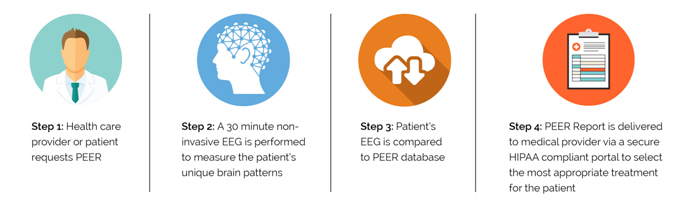

MYnd Analytics, Inc. (the “Company” or "MYnd") employs a clinically validated scalable technology platform to support personalized care for mental health patients. The Company utilizes its patented machine learning, artificial intelligence, data analytics platform for the delivery of telebehavioral health services and its PEER predictive analytics product offering. On November 13, 2017, the Company acquired Arcadian Telepsychiatry Services LLC ("Arcadian"), which manages the delivery of telepsychiatry and telebehavioral health services through a nationwide network of licensed and credentialed psychiatrists, psychologists and master's-level therapists. The Company is commercializing its PEER predictive analytics tool to help physicians reduce trial and error treatment in mental health. MYnd's patented, clinically validated technology platform ("PEER Online") utilizes complex algorithms to analyze electroencephalograms ("EEGs") to generate Psychiatric EEG Evaluation Registry (“PEER”) Reports to predict individual responses to a range of medications prescribed for the treatment of behavioral disorders including depression, anxiety, bipolar disorder, post-traumatic stress disorder (“PTSD”) and other non-psychotic disorders.

The Company entered into an equity purchase agreement (the “Agreement”) with Arcadian and Mr. Robert Plotkin, pursuant to which the Company acquired all of the issued and outstanding membership interests (the “Equity Interests”) of Arcadian from Mr. Plotkin. In consideration for the Equity Interests, the Company entered into an employment agreement with Mr. Plotkin, pursuant to which the Company will continue to employ Mr. Plotkin as the CEO of Arcadian for an annual salary of $215,000, and granted him 35,000 options to purchase common stock of the Company. In addition, the Company entered into the Guaranty (as described below).

In connection with the Agreement, Arcadian entered into the Side Agreement and Seed Capital Amendment with Ben Franklin Technology Partners of Southeastern Pennsylvania ("BFTP"), pursuant to which BFTP waived its rights (a) to an equity conversion contemplated by the existing funding agreements (as they may be amended, supplemented or otherwise modified from time to time, the “BFTP Loan Documents”) between Arcadian and BFTP, under which BFTP has loaned Arcadian, as of August 31, 2017, the aggregate principal amount of $700,000 and upon which an aggregate of $85,496 of interest had then accrued (collectively, the “Loan Amount”) and (b) to act as an observer to Arcadian's board. Under the Side Agreement and Seed Capital Amendment, Arcadian acknowledged and reaffirmed all of BFTP’s claims, encumbrances granted by Arcadian to BFTP, and BFTP’s other rights, interests and remedies pursuant to the BFTP Loan Documents and otherwise. The effectiveness of the Side Agreement and Seed Capital Amendment are conditioned upon (i) Arcadian making a one-time payment to BFTP of $175,000 as payment for the redemption and cancellation of two warrants to purchase equity interests in Arcadian and (ii) the Company entering into a guaranty with respect to Arcadian's obligations (including the Loan Amount) to BFTP under the BFTP Loan Documents, as amended by the Side Agreement and Seed Capital Amendment. Upon satisfaction of the foregoing conditions, the aforementioned BFTP rights will be waived and the BFTP warrants will be cancelled. The Side Agreement and Seed Capital Amendment further provide that following the closing of the transactions contemplated by the Agreement, the Company will be obligated to complete all financial reporting to BFTP required under the BFTP Loan Documents.

In addition, the Company executed an absolute, unconditional, irrevocable and continuing guaranty and suretyship (the “Guaranty”) in favor of BFTP, pursuant to which it unconditionally guaranteed the prompt payment and performance, when due, of all loans (including the Loan Amount), advances, debts, liabilities, obligations, covenants and duties owing by Arcadian to BFTP under the BFTP Loan Documents. Under the Guaranty, if Arcadian defaults under any obligation under the BFTP Loan Documents, the Company will be required to pay the amount then due to BFTP. The Guaranty contains representations, warranties, covenants, conditions, events of default and indemnities that are customary for agreements of this type.

The Market for Telebehavioral Health and Predictive Healthcare

Telebehavioral health services involve the use of video conferencing equipment to conduct real time mental health consultations between a clinician and patient including individuals living in underserved areas or those with limited access to services. Over eighty-nine million Americans live in federally designated Mental Health Professional Shortage Areas. Two-thirds of US primary care physicians report not having adequate access to psychiatric care for their patients. Arcadian facilitates on-demand telebehavioral health services to expedite assessment, diagnosis, treatment, and disposition of patients in a wide variety of settings.

Analysts have identified predictive healthcare as one of the fastest-growing markets in healthcare, particularly, healthcare startups using advanced machine learning algorithms for medical imaging and diagnostics, remote patient monitoring, and risk prediction. The global healthcare analytics market is expected to reach USD $42.8 billion by 2024, according to a report by Grand View Research, Inc. Efforts to reduce the spiraling healthcare costs are facilitating the usage of healthcare analytics. Additionally, the benefits of healthcare analytics include the improvement of patient access to customized care, the furthering of transparent operations to enable better public oversight, and innovation in patient care delivery and services.

3

The Challenge and the Opportunity

The American Psychiatric Association estimates that between $26 billion and $48 billion could be saved annually through effective integration of medical and behavioral health services. Traditional in-person patient encounters for behavioral health are hampered by relative shortages of behavioral health clinicians, especially in areas of the country where there is the greatest need. Arcadian’s customers are payers, health plans, Employee Assistance Programs ("EAPs"), and provider groups. With the benefit of the MYnd technology platform, Arcadian is positioned to capitalize on the need for behavioral health services, overcoming gaps in care access, while supporting healthcare organizations nationwide.

Psychotropic medications have become the dominant treatment for mild to severe behavioral disorders with greater than 400% growth in the prescription of antidepressant medications over the last two decades. However, recent research has emerged challenging the assumption of efficacy of strategies for prescribing psychotropic medications for the treatment of mild to severe behavioral disorders, finding that these medications often do not work or lose their efficacy over time.

Currently, due to the lack of objective neurophysiological data available to physicians of brain function, physicians regularly make prescribing decisions based on incomplete symptomatic factors. To address this unmet medical need, we offer our PEER Online technology to analyze an individual's digital Quantitative EEG (“QEEG”), correlating the individual’s QEEG features with medication outcomes in our proprietary database of over 11,000 unique patients to predict the efficacy of psychotropic medications by class and individual medication. The output of this analysis - the PEER Report - has been used as adjunctive information by physicians for over a decade on patients suffering from behavioral disorders including depression, anxiety disorders, obsessive-compulsive disorder ("OCD"), bipolar disorder, PTSD, addiction and eating disorders, including anorexia.

The Mental Health Parity and Addiction Equity Act (MHPAEA) requires health plans to ensure parity between medical/surgical benefits and mental health/substance use disorder (MH/SUD) benefits. Specifically, plans must offer parity in both numerical or “quantitative” financial requirements or treatment limits (e.g., cost sharing and day or visit limits) and “non-quantitative” treatment limits. This legislation drove a substantial increase in reimbursement transparency: plan administrators must now provide detailed criteria for medical necessity determinations relating to MH/SUD, including prior authorization requirements, determinations that a treatment is experimental, methods for reimbursing providers, step-therapy programs, and restrictions based on geographic location or facility type.

Further, key conditions of the 21st Century Cures Act have recently required the Departments of Labor, Treasury, and Health and Human Services to strengthen their enforcement of the MHPAEA, requiring audits and enforcement actions for any health insurer or group health plan that has violated MHPAEA at least five times.

Milliman Global Actuaries recently released a report on mental health utilization from 2008-13, the period in which the initial Parity regulations were implemented. For commercial health plans, outpatient visits increased by 19.5% for mental health care compared to only 2% for medical-surgical treatments; professional services increased by 9.1% for mental health versus 3.1% for medical-surgical care. In summary, the practical effect of these regulations is that mental health care visits have increased significantly, and we believe that current procedures with existing reimbursement codes such as EEG will be increasingly reimbursed by payers.

Arcadian Telepsychiatry Services LLC

Arcadian Telepsychiatry Services LLC, our wholly owned subsidiary acquired in November 2017, manages the delivery of telebehavioral health services through a multi-state network of licensed and credentialed psychiatrists, psychologists and other behavioral health therapists ("Providers"). Although many companies provide broad telehealth services within the U.S., only a few companies have a primary focus on telepsychiatry and telebehavioral health. Arcadian’s business model is unique, because it has access to a broad network of licensed behavioral health professionals exclusively focused on telepsychiatry and telebehavioral health. These Providers collectively offer a full suite of behavioral health and wellness services, including short-term (urgent), medium-term (rehabilitation) and long-term (management) behavioral care.

Arcadian’s telehealth service delivery model is optimized to deliver behavioral health care anytime and anywhere, offering unprecedented access to behavioral health services. All technology for scheduling and videoconferencing is accessible through a secure portal, creating a seamless experience for the patient, referring physician, and Arcadian provider. The Providers' services include initial and follow-up psychiatric evaluations and diagnoses, medication prescribing and monitoring, urgent on-call evaluations, forensic and legal evaluations, individual and family counseling (e.g., grief, behavior problems, job loss) and drug and alcohol abuse rehabilitation counseling. Arcadian also arranges for services through Employee Assistance Programs (teleEAP) that many employers include as part of their employee benefits packages.

Arcadian contracts for most of its Providers' services through contracts (each a "Service Agreement") with the Providers. Neither the Company nor Arcadian has an ownership interest in any Provider, nor any employment relationships with any Provider. All Providers are required to maintain proper state licensing, credentialing and malpractice insurance. In a typical Service Agreement, Arcadian provides certain management and administrative services in support of the Providers' non-medical functions and the Providers provide telebehavioral health services.

Arcadian and its Providers currently have contracts with 32 insurance companies, human capital management corporations (i.e., EAP benefits), outpatient diagnostic and treatment centers, drug and alcohol rehabilitation centers (outpatient and residential), community behavioral health clinics, treatment and rehabilitation centers, corrections facilities, and post-acute care centers. Arcadian is exploring expansion opportunities by providing services to emergency departments, schools (K-12 and college) and large employers. Arcadian's contracts span from Pennsylvania to California and North Dakota to Louisiana and Texas.

Commercial Strategy

We plan to drive adoption of our technology and secure sustained profitability through the following plan:

| 1. | Continue integration of Arcadian's business into MYnd's technology platform to enable scalable growth and achieve incremental growth through the integration of the MYnd offering with the Arcadian network. We are continuing the integration of Arcadian functions that support scheduling, clinical management and billing operations with the MYnd operating platform to ensure operational efficiency and scalable growth. By doing so, we believe we will have a unique platform which both improves access to and efficacy of behavioral health treatments. |

| 2. | Commercialize PEER through direct marketing to payers, providers and patients. MYnd has implemented a multi-prong strategy to increase patient and provider awareness of the PEER platform involving direct sales, social media and call centers. |

4

| 3. | Continue to pursue military and veterans’ engagements in the US and globally. Due to the high visibility of mental and emotional disorders in their organizations, the military and veterans’ administration possess the ability to sustain demand and need for intervention. We intend to continue the pursue relationships with the military of the United States, Canada and other countries, to improve the condition of those serving and veterans. We have submitted an application for a federal supply schedule solicitation with the Department of Veterans Affairs which, if granted, would provide the Company with a five year General Services Administrative contract with all agencies of the Federal government. The Company has commenced a clinical trial with the Canadian Armed Forces, which will provide both NATO and Health Canada (Canada's single payer system) experience with our PEER technology. It will also increase the size of our data base, and potentially result in PEER being adopted as a standard of care by Health Canada. |

| 4. | Identify and implement strategic opportunities to capitalize on the MYnd technology platform. The Company anticipates that recognition of the utility of the MYnd technology platform will follow with increasing market adoption. Accordingly, we will pursue strategic partnerships, licensing and distribution opportunities with global enterprise customers who provide electronic medical records, prescribing tools, and other large scale clinical management functions. In addition, the Company may evaluate and pursue other strategic opportunities that could prove to be beneficial to the Company's business. |

5

PEER Report and PEER Online Database

A PEER Report is a personalized report for a patient which is generated after the patient receives an EEG. An EEG is a painless, non-invasive test that records the brain's electrical activity and provides a basis for comparison against others within the PEER database. MYnd utilizes AI, machine learning and data analytics in order to inform therapeutic regimens, thereby improving patient outcomes and reducing healthcare costs. The PEER Reports use data from EEG tests, outcomes and machine learning to identify endophenotypic markers of drug response. This big data approach has allowed MYnd to generate a large clinical registry and database of predictive algorithms from more than 11,000 unique patients with psychiatric or addictive problems and 40,000 clinical outcomes.

The PEER Outcomes Database consists of physician-provided assessments of the clinical long-term outcomes of patients and their associated medications. The clinical outcomes of patients are recorded using an industry-standard outcome rating scale, the Clinical Global Impression-Improvement scale (“CGI-I”). The CGI-I allows a clinician to rate how much the patient’s illness has improved or worsened relative to a baseline state. A patient’s illness is compared to change over time and rated as: very much improved, much improved, minimally improved, no change, minimally worse, much worse, or very much worse. The format of the data is standardized and that standard is enforced at the time of capture by a software application. Outcome data is input into the database by the treating physician or their office staff. Each physician has access to their patient data through the software tool that captures the clinical outcome data.

We consider the information contained in the PEER Online database to be a valuable trade secret and are diligent about protecting such information. The PEER Online database is stored on a secure server to which only a limited number of employees have access.

Competitive Advantages of MYnd Technology Platform

MYnd technologies utilizes what is believed to be the largest database of longitudinal patient outcomes, collected from our subscribing physicians and patients over more than a decade. Because our data platform "learns", it supports physicians in personalizing treatment of patients. PEER offers practical advantages to physicians and patients, including:

| • | Scalable and Applicable to Other Services - Our products are built on a secure, HIPAA-compliant Force.com platform which is inherently scalable, i.e. services can be ordered and delivered to any physician with a web browser. The platform is capable of distributing point-of-care data to physicians for new drugs, non-pharmacological treatments, and other findings that are timely and clinically important for clinicians. |

| • | Clinical utility - PEER results are available same-day and provide objective, actionable data to support treating physicians. |

| • | Machine learning - A core attribute of the PEER Registry approach is that it “learns”, using machine learning algorithms to improve the accuracy of recommendations as outcomes are added to the database. |

| • | Higher Efficacy - Findings presented at the Military Health Services Research Symposium in August 2016 included pooled results from all four randomized trials of PEER, with an average 47% improvement (mean change from baseline) for PEER-guided treatments, compared to only 16% average improvement in the standard of care group. In other words, physicians with PEER information in our study had three times higher medication efficacy than physicians treating as usual without the benefit of PEER. |

6

| • | Pharmacogenomics - Currently, we believe that the most proven targets for pharmacogenomics are in the liver - a CYP450 drug metabolism - which apply to less than 15% of Americans. Conversely, PEER is based on functional brain activity and therefore, is more broadly applicable. |

Clinical Results and Independent Validation

PEER has abundant literature showing (1) it affects treatment management decisions, (2) the decisions result in ‘strong’ effects on established measures of effectiveness (>3- fold more than what has been reported by FDA and Cochrane review groups on effects of drugs without benefit of PEER), (3) improved quality of life scores, (4) safety comparable to existing treatment regimens, (5) generalizability to many settings across many types of patients, and (6) substantial cost offsets.

In the 2017 PEER Report Dossier prepared by John Hornberger of Cedar Associates LLC and a Stanford Health Policy Adjunct Affiliate it is stated that "EEG is a well-standardized clinical tool that has been used for decades. As such, the processes for ordering and performing EGG are established and seamless. PEER represents the next logical enhancement, which is to link the automated, quantitative EEG findings with phenotypes (in this case, with drug response in patients with TRD) using the world’s largest clinical repository. The four randomized trials met the essential criteria of showing that PEER increases response rates; because of the strength of randomization, it leads to strong inference that the effect found in the studies were authentic, not due to a confounding factor. Also, the effect was large enough that relatively modest sample were sufficient to demonstrate the effect was very unlikely (less than 1% risk) of being due to random chance alone. In addition, more than 45 studies have shown the feasibility of a well-validated and useful EEG-clinical repository platform to work across many settings and for many types of patients with depression. Due to the high cost of non-response in depression, and the strong effect found in controlled, prospective trials of PEER, use of PEER at its recommended list price represents a substantial cost-saving opportunity for health plans, especially those facing renewed efforts by employers and government agencies to provide and document readily more affordable, value-based care."

Marketing and Sales

The Company will pursue aggressively the expansion of its Arcadian telebehavioral health network, by increasing the number of contracted payors and providers and its geographic reach. The Company will continue to focus marketing efforts on the geographies where there might be fewer available therapists as it continues to develop Arcadian's network. The Company will rely upon its in-house marketing staff to continue to market Arcadian services to insurance companies, EAPs and community behavioral health centers.

The Company will actively pursue cross sales of Arcadian managed care and health system clients. The Company will continue to market paid pilot programs such as the Horizon Blue Cross Blue Shield pilot, while it campaigns for coverage determinations from large health plans and health systems.

The Company also plans to bring this platform to primary care providers, currently the main locus of treatment for behavioral disorders and a physician group that deals every day with the limited access to behavioral health specialists and the poor efficacy of current treatments.

7

Competition

While the telehealth market is in an early stage of development, it is competitive, and we expect it to attract increased competition, which could make it difficult for us to succeed. We currently face competition in the telehealth industry for our solution from a range of companies, including specialized software and solution providers that offer similar solutions, often at substantially lower prices, and that are continuing to develop additional products and becoming more sophisticated and effective. Competition from specialized software and solution providers, health plans and other parties will result in continued pricing pressures, which are likely to lead to price declines, which, in turn, could negatively impact our sales, profitability and market share.

Some of our competitors may have greater name recognition, including Teladoc, MDLive, Doctor on Demand and American Well, longer operating histories and significantly greater resources than we do. Further, our current or potential competitors may be acquired by third parties with greater available resources. As a result, our competitors may be able to respond more quickly and effectively than we can to new or changing opportunities, technologies, standards or customer requirements and may have the ability to initiate or withstand substantial price competition. In addition, current and potential competitors have established, and may in the future establish, cooperative relationships with vendors of complementary products, technologies or services to increase the availability of their solutions in the marketplace. Accordingly, new competitors or alliances may emerge that have greater market share, a larger customer base, more widely adopted proprietary technologies, greater marketing expertise, greater financial resources and larger sales forces than we have, which could put us at a competitive disadvantage. Our competitors could also be better positioned to serve certain segments of the telehealth market, which could create additional price pressure. In light of these factors, even if our solution is more effective than those of our competitors, current or potential clients may accept competitive solutions in lieu of purchasing our solution. If we are unable to successfully compete in the telehealth market, our business, financial condition and results of operations could be materially adversely affected.

Although we are not aware of any company that offers a service directly comparable to PEER Online services, several companies having greater financial and other resources than the Company have suggested that they may be pursuing similar strategies, including Assurerx, Genomind, Verily, IBM Corporation and Google. All of these companies have reported developing either a genomic-based test strategy or other AI analysis of the health metrics to aid treatment.

Intellectual Property

Covering The Use Of The PEER Online Database

We have 20 issued patents, of which seven are in the U.S., at least one of which covers the process of using the data presented in our PEER Online service. Our patents will expire between January 2018 and April 2023 and cover QEEG (quantitative electrophysiology). We have been issued patents in the following countries and regions: Canada (three patents), Europe (two patents), Australia (three patents), Mexico (two patents), Japan (two patents) and Israel (one patent). We also have filed multiple additional patent applications for our technology in the U.S., Europe and Canada.

One US patent approval was for a distinctly new patent estate, covering internet transmission of neurometric information. This new allowance under its basic methods patent portfolio, patent number 8,239,013, covers remote or web-based transmission of neurometric data.

8

During 2009 and 2011, we were awarded additional process patents for use of PEER Online technology in drug discovery, including clinical trial and drug efficacy studies. In addition, we successfully defended our patents by requesting reexamination of a patent issued to Aspect Medical (acquired by Covidien, plc.), resulting in a reduction and narrowing of claims awarded under the previously issued Aspect Medical patents.

Transcranial Magnetic Stimulation

MYnd has filed patent applications in the U.S. and Canada related to the Company's acquisition of patient responsivity data for Transcranial Magnetic Stimulation (“TMS”). This would be the Company's first application for a neurometric predictor of a non-drug therapy. The Company anticipates using this methodology to help physicians better understand which patients may positively respond to TMS for treating depression. The U.S. and Canadian patent applications are entitled “Method for Assessing the Susceptibility of a Human Individual Suffering from a Psychiatric or Neurological Disorder to Neuromodulation Treatment.”

TMS is a non-invasive outpatient procedure that uses magnetic fields to stimulate areas of the brain thought to control mood. TMS is sometimes used as an alternative treatment for patients who have failed one or more antidepressants for the treatment of depression. While treatment periods vary by patient, a typical treatment regimen generally involves 20 to 30 treatments over a four to six week period. TMS responsivity data, which is based on QEEG, helps physicians learn how patients with similar EEG patterns responded to TMS, thereby enabling them to more effectively guide patients most likely to benefit from this treatment and reduce expenditures on patients for whom TMS is not likely to be an effective solution for their depression.

Trademarks

“rEEG”, “PEER Online” (web-based software application), “PEER Online” (web-based services), and “MYnd Analytics” (word mark) are registered trademarks of the Company in the United States. We will continue to expand our brand names and our proprietary trademarks worldwide as our operations expand.

Government Regulation

Arcadian

The healthcare industry, including behavioral healthcare, is extensively regulated at both the state and federal levels. The laws and rules on the practice of behavioral healthcare and telehealth continue to evolve, and the Company will devote significant resources to monitoring these developments. As the applicable laws and rules change, Arcadian must conform its business processes from time to time to be in compliance with these changes.

Provider Licensing, Corporate Practice Restrictions, Certification and Scope of Practice

The practice of health care professions, including the provision of behavioral health services, is subject to various federal, state and local certification and licensing laws, regulations and approvals, relating to, among other things, the adequacy of health care, the practice of medicine and other health professions (including the provision of remote care and cross-coverage practice), equipment, personnel, operating policies and procedures and the prerequisites for prescribing medication. In addition, the provision of health care services through any kind of clinic, facility, storefront or other location open to the public is often subject to state clinic licensure laws akin to those that health facilities like hospitals, surgery centers and urgent care clinics must obtain and maintain. The Company does not operate or promote any physical place to obtain healthcare and therefore does not believe it is subject to any clinic licensure requirements, but the application of some of these laws to the Company and telehealth is unclear and subject to differing interpretation.

Some states have enacted regulations specific to providing services to patients via telehealth. Such regulations include informed consent requirements that some states require providers to obtain from their patients before providing telehealth services. Behavioral health professionals who provide professional services using telehealth modalities must, in most instances, hold a valid license to practice the applicable health profession in the state in which the patient is located. In addition, certain states require a physician providing telepsychiatry to be physically located in the same state as the patient. Arcadian requires each Provider to put in place procedures to ensure that the Provider is in compliance with all applicable laws and regulations. Nevertheless, any failure to comply with these laws and regulations could result in civil or criminal penalties against Arcadian.

Corporate Practice; Fee-Splitting

Arcadian contracts with Providers to help make their psychiatric, psychological and other behavioral health services available to customers. In addition, Arcadian provides a wide range of services to Providers, and the Providers pay Arcadian for those services. These contractual relationships are subject to various state laws, including those in New York, Texas and California, that prohibit professionals from sharing a portion of their professional fees with nonprofessionals (i.e., fee-splitting) and prohibit the practice of medicine or another health profession by lay entities or persons (i.e., corporate practice restrictions) and are intended to prevent unlicensed persons from interfering with or influencing a professional's judgment.

9

State corporate practice and fee-splitting laws vary from state to state and are not consistent among states. In addition, these requirements are subject to broad powers of interpretation and enforcement by state regulators and the courts. may apply to Arcadian if a Provider is licensed there. Accordingly, administrative and management services provided by Arcadian to the Providers, such as scheduling, contracting, setting rates and the hiring and management of clinical personnel, may be considered an element of the practice of a health profession under certain state corporate practice doctrines. Decisions and activities may be viewed by regulatory authorities or other parties, including the Providers, as violating these fee-splitting and the corporate practice restrictions on of the health profession. An adverse finding with respect to fee-splitting and corporate practice restrictions could lead to judicial or administrative action against Arcadian or its Providers, civil or criminal penalties, receipt of cease and desist orders from state regulators, loss of Provider licenses, or the need to revise Service Agreements all in ways that may interfere with Arcadian’s business, cause other materially adverse consequences and may cause a substantial disruption to Arcadian’s business model.

Federal and State Fraud and Abuse Laws

Federal and State Anti-Kickback Statutes

The Company must comply with the federal and state anti-kickback statutes. The federal Anti-Kickback Statute is broadly worded and prohibits the knowing and willful offer, payment, solicitation or receipt of any form of remuneration in return for, or to induce, (i) the referral of a person covered by Medicare, Medicaid or other federal governmental programs, (ii) the furnishing or arranging for the furnishing of items or services reimbursable under Medicare, Medicaid or other federal governmental programs or (iii) the purchasing, leasing or ordering or arranging or recommending purchasing, leasing or ordering of any item or service reimbursable under Medicare, Medicaid or other federal governmental programs. Certain federal courts have held that the federal Anti-Kickback Statute can be violated if “one purpose” of a payment is to induce referrals. In addition, a person or entity does not need to have actual knowledge of this statute or specific intent to violate it to have committed a violation, making it easier for the government to prove that a defendant had the requisite state of mind or “scienter” required for a violation. Moreover, the government may assert that a claim including items or services resulting from a violation of the federal Anti-Kickback Statute constitutes a false or fraudulent claim for purposes of the False Claims Act, as discussed below. Violations of the federal Anti-Kickback Statute may result in exclusion from Medicare, Medicaid or other federal governmental programs as well as civil and criminal penalties, including fines of $50,000 per violation and three times the amount of the unlawful remuneration. Imposition of any of these remedies could have a material adverse effect on our business, financial condition and results of operations.

State anti-kickback statutes require compliance independent of the federal Anti-Kickback Statute. Some state anti-kickback statutes prohibit the same conduct as the federal Anti-Kickback Statute, but may apply the prohibition broadly to all payor-reimbursed services, not just those that are federally funded. Other state anti-kickback statutes are limited to Medicaid services, while still others apply only to patient referrals and not to actions that involve “arranging or recommending” healthcare items or services. Very few state anti-kickback statutes have the extensive safe harbors and regulatory guidance of the federal Anti-Kickback Statute, making interpretation of the scope of the statutes more uncertain than the federal Anti-Kickback Statute. Like the federal Anti-Kickback Statute, violations of most state anti-kickback laws are subject to criminal sanctions. Accordingly, the Company must analyze and ensure that it complies with state anti-kickback statutes whenever it commences operations in a new state. Any violation of state anti-kickback laws, therefore, could have a material adverse effect on our business, financial condition and results of operations.

Physician Self-Referral Laws

There is a federal physician self-referral prohibition, commonly known as the Stark Law, which prohibits a physician from referring Medicare patients to an entity providing “designated health services” if the physician or a member of such physician’s immediate family has a “financial relationship” with the entity, unless an exception applies. We do not believe the Company’s operations, including those of Arcadian, implicate the Stark Law, because neither the Company nor Arcadian nor the Providers acting pursuant to the Services Agreements offer or provide any services that would be considered designated health services under the Stark Law. As with the anti-kickback laws, however, physician self-referral prohibitions exist at the state level and, like the Stark Law, apply civil penalties to violations of their terms. These state physician self-referral laws are often similar to the Stark Law, but may apply to different services than the Stark Law and may have different exceptions. The Company does not believe it is noncompliant with any state physician self-referral laws, but these laws are often vague, subject to amendment and lacking in court precedent or regulatory guidance. It is possible, therefore, that now or in the future the Company could be found to be out of compliance with one or more state physician self-referral laws. Any such noncompliance could have a material adverse effect on our business, financial condition and results of operations.

10

Federal and State False Claims Statutes

Both federal and state government agencies have continued civil and criminal enforcement efforts as part of numerous ongoing investigations of healthcare companies and their executives and managers. Although there are a number of civil and criminal statutes that can be applied to healthcare providers, a significant number of these investigations involve the federal False Claims Act. These investigations can be initiated not only by the government, but also by a private party asserting direct knowledge of fraud. These “qui tam” whistleblower lawsuits may be initiated against any person or entity alleging such person or entity has knowingly or recklessly presented, or caused to be presented, a false or fraudulent request for payment from the federal government, or has made a false statement or used a false record to get a claim approved. In addition, the improper retention of an overpayment for 60 days or more is also a basis for a False Claim Act action, even if the claim was originally submitted appropriately. Penalties for False Claims Act violations include fines ranging from $5,500 to $11,000 for each false claim, plus up to three times the amount of damages sustained by the federal government. A False Claims Act violation may provide the basis for exclusion from government-funded healthcare programs.

In addition, some states have laws similar to the False Claims Act. The scope of these laws and the interpretations of them vary from state to state and are enforced by state courts and regulatory authorities, each with broad discretion. Some state false claims laws apply to claims for health care or services submitted to any third-party payor, including commercial insurers, not just those reimbursed by a government-funded healthcare program. A determination of liability under such state false claims laws could result in fines and penalties and restrictions on the Company’s ability to operate in these jurisdictions and have a material adverse effect on our business, financial condition and results of operations.

Other Healthcare Anti-Fraud Laws

The federal Health Insurance Portability and Accountability Act of 1996, as amended by the Health Information Technology for Economic and Clinical Health Act, or HITECH, and their implementing regulations, collectively referred to as HIPAA, established several separate crimes for making false or fraudulent claims to insurance companies and other governmental payors of healthcare services. Under HIPAA, these two additional federal crimes are: “Healthcare Fraud” and “False Statements Relating to Healthcare Matters.” The Healthcare Fraud statute, 18 U.S.C. § 1347, prohibits knowingly and willfully executing or attempting to execute a scheme or artifice to defraud any healthcare benefit program, including private payors, or obtaining by means of false or fraudulent pretenses, representations or promises any of the money of the healthcare benefit program in connection with the delivery of, or payment for, healthcare benefits, items or services. A violation of this statute may result in fines, imprisonment or exclusion from government-sponsored healthcare programs. The False Statements Relating to Healthcare Matters statute, 18 U.S.C. § 1035, prohibits knowingly and willfully falsifying, concealing or covering up a material fact by any trick, scheme or device, making any materially false, fictitious or fraudulent statement or representation, or making or using any materially false writing or document knowing that it contains any materially false, fictitious, or fraudulent statement or entry, in connection with the delivery of or payment for healthcare benefits, items or services. A violation of this statute may result in fines or imprisonment. This statute could be used by the government to assert criminal liability if a healthcare provider knowingly fails to refund an overpayment. These provisions target some of the same conduct in the submission of claims to private payors as the federal False Claims Act covers in connection with governmental health programs.

In addition, the federal Civil Monetary Penalties Law imposes civil administrative sanctions for, among other violations, inappropriate billing of services to federally funded healthcare programs and employing or contracting with individuals or entities who are excluded from participation in federally funded healthcare programs. Moreover, a person who offers or transfers to a Medicare or Medicaid beneficiary any remuneration, including waivers of co-payments and deductible amounts (or any part thereof) that the person knows or should know is likely to influence the beneficiary’s selection of a particular provider, practitioner or supplier of Medicare or Medicaid payable items or services may be liable for civil monetary penalties of up to $10,000 for each wrongful act. Moreover, in certain cases, providers who routinely waive copayments and deductibles for Medicare and Medicaid beneficiaries can also be held liable under the federal Anti-Kickback Statute and civil False Claims Act, which can impose additional penalties associated with the wrongful act.

11

Any violation of these other healthcare fraud laws could have a material adverse effect on our business, financial condition and results of operations.

12

State and Federal Health Information Privacy and Security Laws

There are numerous U.S. federal and state laws and regulations related to the privacy and security of personally identifiable information, or PII, including health information. In particular, HIPAA establishes privacy and security standards that limit the use and disclosure of protected health information, or PHI, and requires the implementation of administrative, physical, and technical safeguards to ensure the confidentiality, integrity and availability of individually identifiable health information in electronic form. Arcadian’s Providers and some of its clients are all regulated as covered entities under HIPAA. Since the effective date of the HIPAA Omnibus Final Rule on September 23, 2013, HIPAA’s requirements are also directly applicable to the independent contractors, agents and other “business associates” of covered entities that create, receive, maintain or transmit PHI in connection with providing services to covered entities. Arcadian is a business associate under these requirements.

Violations of HIPAA may result in civil and criminal penalties. The civil penalties range from $100 to $50,000 per violation, with a cap of $1.5 million per year for violations of the same standard during the same calendar year. However, a single breach incident can result in violations of multiple standards. HIPAA also contains a breach notification rule. Under the breach notification rule, covered entities must notify affected individuals without unreasonable delay in the case of a breach of unsecured PHI, which may compromise the privacy, security or integrity of the PHI. In addition, notification must be provided to the HHS and the local media in cases where a breach affects more than 500 individuals. Breaches affecting fewer than 500 individuals must be reported to HHS on an annual basis. The regulations also require business associates of covered entities to notify the covered entity of breaches by the business associate.

State attorneys general also have the right to prosecute HIPAA violations committed against residents of their states. Although HIPAA does not create a private right of action that would allow individuals to sue in civil court for a HIPAA violation, its standards have been used as the basis for the duty of care in state civil suits, such as those for negligence or recklessness in misusing personal information. In addition, HIPAA mandates that HHS conduct periodic compliance audits of HIPAA covered entities and their business associates for compliance. It also tasks HHS with establishing a methodology whereby harmed individuals who were the victims of breaches of unsecured PHI may receive a percentage of the Civil Monetary Penalty fine paid by the violator. In light of the HIPAA Omnibus Final Rule, recent enforcement activity, and statements from HHS, we expect increased federal and state privacy and security enforcement efforts.

Many states also have laws that protect the privacy and security of sensitive and personal information, including health information. These laws may be similar to or even more protective than HIPAA and other federal privacy laws. Where state laws are more protective than HIPAA, Arcadian must comply with the state laws, in addition to HIPAA. In certain cases, it may be necessary to modify Arcadian's planned operations and procedures to comply with these more stringent state laws. Not only may some of these state laws impose fines and penalties upon violators, but also some, unlike HIPAA, may afford private rights of action to individuals who believe their personal information has been misused.

In addition to HIPAA, state health information privacy and state health information privacy laws, Arcadian may be subject to other state and federal privacy laws, including laws that prohibit unfair privacy and security practices and deceptive statements about privacy and security and laws that place specific requirements on certain types of activities, such as data security and texting.

In recent years, there have been a number of publicized data breaches involving the improper use and disclosure of PII and PHI. Many states have responded to these incidents by enacting laws requiring holders of personal information to maintain safeguards and to take certain actions in response to a data breach, such as providing prompt notification of the breach to affected individuals and state officials. In addition, under HIPAA and pursuant to the related contracts that we enter into with our business associates, we must report breaches of unsecured PHI to our contractual partners following discovery of the breach. Notification must also be made in certain circumstances to affected individuals, federal authorities and others.

Any violation of HIPAA or state privacy laws, therefore, could result in civil or even criminal liability, subject us to significant monetary fines, require us to restructure our operations and otherwise have a material adverse effect on our business, financial condition and results of operations.

FDA Regulation

The PEER Outcome database is registered with the United States Food and Federal Drug Administration ("FDA") and the State of California as a Class I Exempt Device within the category of Medical Device Data System.

13

We currently intend to continue marketing as a cloud-based neurometric information service branded as PEER Online ("neurometric services"), under our Class I registration, while we continue to pursue the military trial and consider submission of a Class II device premarket notification. If we continue to market PEER Online and the FDA determines that we should be subject to further FDA regulation, it could seek enforcement action against us based upon a position that our PEER Online product represents a Class II medical device, as a result of which we could be forced to cease our marketing activities and pay fines and penalties. In August 2012, the FDA reviewed the study protocol to use our PEER Interactive Product, which is substantially similar to the PEER Online product, and determined that the Walter Reed PEER Trial was considered a Non-Significant Risk ("NSR") clinical trial and did not require an Investigational Device Exemption.

In addition to the foregoing, federal and state laws and regulations relating to the sale of our neurometric services are subject to future changes, as are administrative interpretations of regulatory agencies. In the event that federal and state laws and regulations change, we may need to incur additional costs to seek government approvals for the sale of our neurometric services.

Employees

As of September 30, 2018, our operation has twenty–one full-time employees. We believe that our relations with our employees are good. None of our employees belong to a union.

Corporate Background

The Company was incorporated in Delaware on March 20, 1987, under the name Age Research, Inc. Prior to January 16, 2007, the Company (then called Strativation, Inc.) existed as a “shell company” with nominal assets whose sole business was to identify, evaluate and investigate various companies to acquire or with which to merge. On January 16, 2007, we entered into an Agreement and Plan of Merger with CNS Response, Inc., a California corporation formed on January 11, 2000 (“CNS California”), and CNS Merger Corporation, a California corporation and our wholly-owned subsidiary (“MergerCo”) pursuant to which we agreed to acquire CNS California in a merger transaction wherein MergerCo would merge with and into CNS California, with CNS California being the surviving corporation (the “Merger”). On March 7, 2007, the Merger closed, CNS California became our wholly-owned subsidiary, and on the same date we changed our corporate name from Strativation, Inc. to CNS Response, Inc.

At the meeting of shareholders of CNS Response, Inc. held on October 28, 2015, the shareholders approved a proposal to change the Company’s name to MYnd Analytics, Inc. The Company’s charter was amended on November 2, 2015.

The Company actively operates its businesses through MYnd Analytics, Inc. (California) (formerly called CNS Response, Inc. (California) until November 22, 2017) and, until September 30, 2012, also operated the Neuro-Therapy Clinic, Inc. (“NTC”), which was acquired as a wholly-owned subsidiary in January 2008, when it was the Company’s largest customer.

Our current address is 26522 La Alameda, Suite 290, Mission Viejo, California 92691. Our telephone number is (949) 420-4400 and we maintain a website at www.MYndAnalytics.com. The reference to our web address does not constitute incorporation by reference of the information contained at this site.

14

INVESTING IN MYND ANALYTICS, INC. INVOLVES A HIGH DEGREE OF RISK. YOU SHOULD CAREFULLY CONSIDER THE FOLLOWING RISK FACTORS AND ALL OTHER INFORMATION CONTAINED IN THIS REPORT BEFORE PURCHASING OUR COMMON STOCK. THE RISKS AND UNCERTAINTIES DESCRIBED BELOW ARE NOT THE ONLY ONES FACING US. ADDITIONAL RISKS AND UNCERTAINTIES THAT WE ARE UNAWARE OF, OR THAT WE CURRENTLY DEEM IMMATERIAL, ALSO MAY BECOME IMPORTANT FACTORS THAT AFFECT US. IF ANY OF THE FOLLOWING RISKS OCCUR, OUR BUSINESS, FINANCIAL CONDITION OR RESULTS OF OPERATIONS COULD BE MATERIALLY AND ADVERSELY AFFECTED. IN THAT CASE, THE TRADING PRICE OF OUR COMMON STOCK COULD DECLINE, AND YOU MAY LOSE SOME OR ALL OF THE MONEY YOU PAID TO PURCHASE OUR COMMON STOCK.

Risks Related to Our Company

We need immediate additional funding to support our operations and capital expenditures, which may not be available to us. This lack of availability could result in the cessation of our business. Our recurring net losses and negative cash flows from operations raise substantial doubt about our ability to continue as a going concern.

We have not generated significant revenues or become profitable, may never do so and may not generate sufficient working capital to cover costs of operations. Our recurring net losses and negative cash flows from operations raise substantial doubt about our ability to continue as a going concern. Historically, we have been unable to pay other obligations as they become due and have been in arrears on paying certain of our larger creditors. We have a history of insolvency that requires us to immediately secure additional funds to continue our operations. Until we can generate a sufficient amount of revenues to finance our operations and capital expenditures, we are required to finance our cash needs primarily through public or private equity offerings, debt financings, borrowings or strategic collaborations. As of September 30, 2018, we had approximately $3.3 million in cash and cash equivalents on hand. We will therefore need additional funds to continue our operations and will need substantial additional funds before we can increase demand for our telebehavioral health services and PEER solution offering.

As of September 30, 2018, the Company has issued purchase notices to Aspire Capital under a common stock purchase agreement with Aspire Capital dated as December 6, 2016 (the "First Purchase Agreement") to purchase an aggregate of 1,180,000 shares of common stock, at a per share price of $2.00, resulting in gross cash proceeds of approximately $2.4 million. As of September 30, 2018, the Company has issued purchase notices to Aspire Capital under the second common stock purchase agreement with Aspire Capital dated as of May 15, 2018 (the "Second Purchase Agreement") to purchase an aggregate of 884,671 shares of common stock, resulting in gross cash proceeds of approximately $1.9 million. On November 26, 2018, the Company received shareholder approval to remove the exchange cap under the Second Purchase Agreement in compliance with the applicable listing rules of the Nasdaq Stock Market. Pursuant to Nasdaq Listing Rule 5635(d), shareholder approval is required prior to the issuance of securities in connection with a transaction other than a public offering involving the sale, issuance or potential issuance by the Company of common stock (or securities convertible into or exercisable common stock) equal to 20% or more of the common stock outstanding before the issuance for less than the greater of book or market value of the stock. Following receipt of shareholder approval, the Company may issue an additional $8.1 million, up to an aggregate of $10 million, of common stock to Aspire Capital under the Second Purchase Agreement. The issuance of shares of common stock that were issued from time to time to Aspire Capital under the First and Second Purchase Agreement were exempt from registration under the Securities Act, pursuant to the exemption for transactions by an issuer not involving any public offering under Section 4(a)(2) of the Securities Act.

When we elect to raise additional funds or additional funds are required, we may raise such funds from time to time through public or private equity offerings, debt financings, corporate collaboration and licensing arrangements or other financing alternatives, as well as through sales of common stock to Aspire Capital under the First Purchase Agreement or Second Purchase Agreement. Additional equity or debt financing or corporate collaboration and licensing arrangements may not be available on acceptable terms, if at all. If we are unable to raise additional capital in sufficient amounts or on terms acceptable to us, we will be prevented from pursuing acquisition, licensing, development and commercialization efforts and our ability to generate revenues and achieve or sustain profitability will be substantially harmed.

We are currently exploring additional sources of capital; however, we do not know whether additional funding will be available on acceptable terms, or at all, especially given the economic conditions that currently prevail. Furthermore, any additional equity funding will likely result in significant dilution to existing stockholders, and, if we incur additional debt financing in the future, a substantial portion of our operating cash flow may be dedicated to the payment of principal and interest on such indebtedness, thus limiting funds available for our business activities. If adequate funds are not available, it would have a material adverse effect on our business, financial condition and/or results of operations and could cause us to be required to cease operations. Our financial statements include an opinion of our auditors that our recurring net losses and negative cash flows from operations raise substantial doubt about our ability to continue as a going concern.

15

Our independent registered public accounting firm has expressed substantial doubt about our ability to continue as a going concern.

We have experienced significant net losses and sustained negative cash flows from operations. In the twelve months ended September 30, 2018, we incurred a net loss of $10.3 million and used cash for operating activities of $9.0 million. We had an accumulated deficit of $85.2 million as of September 30, 2018. We expect to experience further significant net losses in 2018 and the foreseeable future. These factors raise substantial doubt about our ability to continue as a going concern for at least the next twelve months from the date of the issuance of the financial statements. As of and for the year ended September 30, 2018, our independent registered public accounting firm has included an explanatory paragraph in their audit report raising substantial doubt about our ability to continue as a going concern. Our consolidated financial statements do not include any adjustments that may result from the outcome of this uncertainty. If we are unable to obtain adequate funding from this proposed offering or in the future, or if we are unable to grow our revenue substantially to achieve and sustain profitability, amongst other factors, we may not be able to continue as a going concern, and our shareholders may lose some or all of their investment in us.

We have a history of operating losses and we have never been profitable.

Since our inception, we have incurred significant operating losses. As of September 30, 2018, our accumulated deficit was approximately $85.2 million. On November 13, 2017, we acquired Arcadian, a telepsychiatry and telebehavioral health company. Arcadian also has a history of significant operating losses, which represent a further obstacle to our goal of achieving profitability.

Our future capital requirements will depend on many factors, such as the risk factors described in this section, including our ability to maintain our existing cost structure and to execute our business and strategic plans, including the successful integration of the PEER solution offering with the Arcadian network. Even if we achieve profitability, we may be unable to maintain or increase profitability on a quarterly or annual basis.

Risks Related to Our Business-Telebehavioral Health

Our telebehavioral health business could be adversely affected by new state actions relating to healthcare services and telemedicine providers, which could restrict our ability to provide the full range of our services in certain states.

Our ability to conduct business in each state is dependent upon the state's treatment of telehealth under each state's laws, rules and policies governing the practice of medicine and other health care professions, which are subject to changing political, regulatory and other influences. Some state professional boards have established new rules or interpreted existing rules in a manner that limits or restricts our ability to conduct our business as currently conducted in other states, and it is possible that the laws and rules governing the practice of telehealth in one or more states may change in a similar manner in the future. Many states have imposed different, and, in some cases, additional, standards regarding the provision of services via telehealth. These standards often relate to particular modalities of telecommunication that are permitted or prohibited, meaning that a system the Company has established in some states may not satisfy regulatory requirements in others. State laws are also in flux regarding the licensure required to provide services via telehealth. By way of example, certain state Medicaid programs may cover behavioral health treatment provided by psychiatric nurse practitioners, but not clinical social workers. Others provide that certain services can be provided via telehealth by a clinical social worker, but not a licensed mental health counselor. Finally, both federal and state laws impose strict standards on using telehealth to prescribe certain classes of controlled substances that can be commonly used to treat behavioral health disorders. Recently passed federal legislation will also allow for controlled substances to be prescribed in emergency situations to treat substance use disorder, and if that change results in further abuse of controlled substances instead of curbing their abuse as intended, there could be negative ramifications for the entire telebehavioral health industry. The unpredictability of this regulatory landscape means that sudden changes in policy regarding standards of care and reimbursement are possible. If this were to happen, and we were unable to adapt our business model accordingly, our operations in such states could be disrupted, which could have a material adverse effect on our business, financial condition and results of operations. Federal law prohibits prescribing controlled substances without a prior in-person examination unless one of a number of narrow exceptions is met, and certain states impose further restrictions which prohibit prescribing certain classes of controlled substances via telemedicine altogether.

Our telebehavioral health business is dependent on our relationships with affiliated professional entities, which we do not own, to provide physician services, and our business would be adversely affected if those relationships were disrupted.

There is a risk that state authorities in some jurisdictions may find that our contractual relationships with our affiliated physicians, psychologists and other behavioral health professionals ("Providers") violate laws prohibiting the corporate practice of medicine and certain other health professions. These laws generally prohibit the practice of medicine and certain other health professions by lay persons or entities and are intended to prevent unlicensed persons or entities from interfering with or inappropriately influencing the clinician's professional judgment. The professions subject to corporate practice restrictions and the extent to which each state considers particular actions or contractual relationships to constitute improper influence of professional judgment vary across the states and are subject to change and evolving interpretations by state boards of medicine and other health professions and state attorneys general. As such, we must monitor our compliance with laws in every jurisdiction in which we operate on an ongoing basis and we cannot guarantee that subsequent interpretation of the corporate practice laws will not further circumscribe our business operations. State corporate practice restrictions also often impose penalties on health professionals for aiding a corporate practice violation, which could discourage clinicians from participating in our network of providers. Any difficulty securing clinicians to participate in our network could impair our ability to provide telebehavioral health services and could have a material adverse effect on our business.

16

Corporate practice restrictions exist in some form, whether by statute, regulation, professional board or attorney general guidance, or case law, in at least 42 states, though the broad variation between state application and enforcement of the doctrine makes establishing an exact count difficult. Because of the prevalence of corporate practice restrictions on medicine and psychology in particular, including in the states where we predominantly conduct our business, we contract for provider services through services agreements rather than employ Providers. We expect that these relationships will continue, but we cannot guarantee that they will. A material change in our relationship with the Providers, whether resulting from a dispute among the entities, a change in government regulation, or the loss of these affiliations, could impair our ability to provide telebehavioral health services and could have a material adverse effect on our business, financial condition and results of operations.

Evolving government regulations may require increased costs or adversely affect our results of operations.

In a regulatory climate that is uncertain, our operations may be subject to direct and indirect adoption, expansion or reinterpretation of various laws and regulations. Compliance with these future laws and regulations may require us to change our practices at an undeterminable and possibly significant initial monetary and annual expense. These additional monetary expenditures may increase future overhead, which could have a material adverse effect on our results of operations.

We have identified what we believe are the areas of government regulation that, if changed, would be costly to us. These include: rules governing the practice of telehealth; including the remote prescribing of controlled substance; licensure standards for behavioral health professionals; laws limiting the corporate practice of medicine and other professions; clinic licensure laws requiring health facilities to obtain a clinic license; fraud and abuse; reimbursement and false claims statutes and regulations governing the submission of health care claims; cybersecurity and privacy laws; laws and rules relating to the distinction between independent contractors and employees; and tax and other laws encouraging employer-sponsored health insurance. There could be laws and regulations applicable to our business that we have not identified or that, if changed, may be costly to us, and we cannot predict all the ways in which implementation of such laws and regulations may affect us.

In the states in which we operate, we believe we are in compliance with all applicable regulations, but, because of the uncertain regulatory environment, certain states may determine that we are in violation of their laws and regulations. If we must remedy such violations, we may be required to modify our services and solutions in such states in a manner that undermines our solution’s attractiveness to patients or providers. We may become subject to fines or other penalties or, if we determine that the requirements to operate in compliance in such states are overly burdensome, we may elect to terminate our operations in such states. In each case, our revenue may decline and our business, financial condition and results of operations could be materially adversely affected.

Additionally, the introduction of new services may require us to comply with additional, yet undetermined, laws and regulations. Compliance may require restructuring our relationships with Providers, increasing our security measures and expending additional resources to monitor developments in applicable rules and ensure compliance. The failure to adequately comply with these future laws and regulations may delay or possibly prevent some of our solutions or services from being offered, which could have a material adverse effect on our business, financial condition and results of operations.

The telebehavioral health market is immature and volatile, and if it does not develop, if it develops more slowly than we expect, if it encounters negative publicity or if our solution does not drive patient engagement, the growth of our business will be harmed.